'Buy the Umbrella' - Issue #20

Hi there!

Here is your latest dose of “Buy the Umbrella”, a short list of interesting things I’ve been reading and thinking about during the week.

Tweet

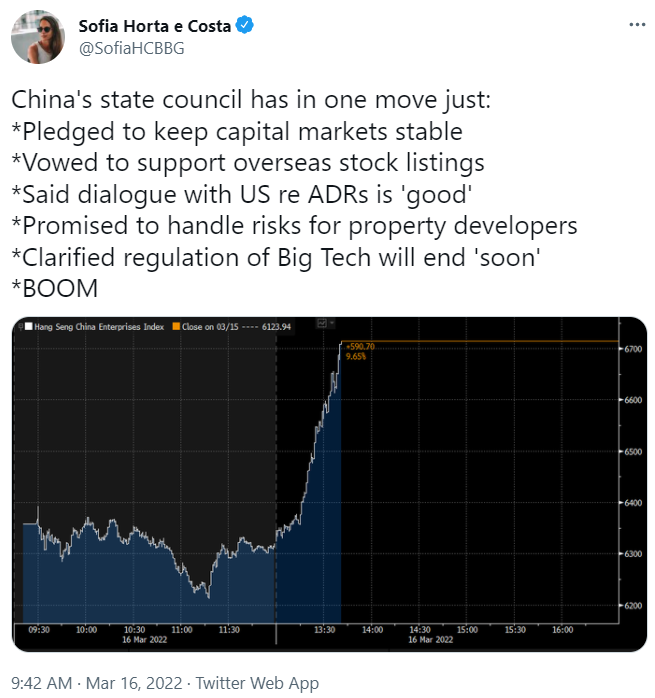

Chinese equity markets have performed poorly since their February 2021 peak, down 41.5% and have significantly underperformed relative to global indices.

As a result, sentiment towards Chinese equities has become incredibly negative, to the extent that J.P. Morgan analysts labelled Chinese internet names as "uninvestable" on Tuesday 15th March.

Less than 24 hours later, Chinese stocks leaped on news that the State Council has pledged to support the economy and capital markets. This could potentially put a floor under those sectors hurt by the regulatory crackdown. Since then, the Hang Seng index is up 16.5%.

Even after this rebound, Alibaba and Tencent continue to trade at steep discounts to their historical averages, largely due to the regulatory crackdown. Alibaba is trading at an EV/EBITDA of 10.9x versus its average of 33.1x since its 2014 IPO, while Tencent is trading at 11.6x versus its average of 26.8x since its 2004 IPO.

Quotes

“The stock market is a device for transferring money from the impatient to the patient.”

— Warren Buffett

“One of the worst things about ideology is that it makes people attribute problems to the wrong causes. E.g. plagues are caused by sin. This is easier to see in history, but it still happens all the time. And if you get the cause wrong, you have no hope of fixing the problem.”

— Paul Graham

Charts

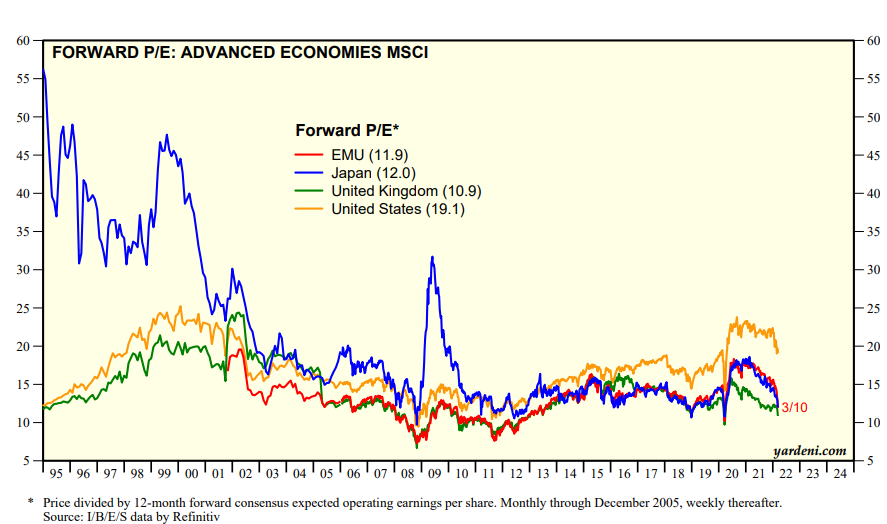

With the recent correction in global equity markets, it is helpful to zoom out to get a better idea of where valuations stand relative to historical levels.

Evidently, the gap between U.S. equity valuations (based on Price/Forward 12-month Earnings ratio) and other developed markets continues to be the largest in decades. What are the odds that the U.S. can sustain this premium given it trades above its historical average?

Within emerging markets, India's equity valuations stand out as they are currently even more expensive than the U.S (20.0x vs. 19.1x).

Interestingly, China trades at 10.1x, below its historical average of around 12x. J.P. Morgan have put together a handy detailed deck on the economy and equity market valuations.

Articles

'Buy-now, pay-later'

Affirm, the U.S.-based 'buy-now, pay-later' company, typically lends small loans to their customers which it then packages and sells off to investors as asset-back securities (ABS). Last Friday, the company was forced to delay its proposed $500m ABS sale according to Bloomberg.

A major investor in the top-rated 'AAA' portion of the deal was said to have backed out at the last minute forcing the transaction to be halted.

Affirm is a relatively new seller in the ABS market, having only been active since July 2020, executing just eight deals and therefore lacks a track record during more turbulent backdrops.

Unsurprisingly, U.S. regulators have started to take an unfavourable view of the business model due to concerns over encouraging consumers to accumulate too much debt.

Saudi Arabia considers accepting yuan instead of dollars for Chinese oil sales

WSJ reports that the world's top crude exporter is in active talks with Beijing to price some of its oil sales to China in yuan. This potentially significant move would impact the U.S. dollar's dominance of the global petroleum market and mark another shift by Saudi Arabia towards Asia.

In 2018, China introduced yuan-priced oil contracts as part of its efforts to make its currency tradable across the world, but they have yet to gain real traction. For China, dependence on dollars has become a concern given U.S. sanctions on Iran over its nuclear program, and on Russia in response to the Ukraine invasion.

Notably, the talks have been going on for six years but have allegedly accelerated this year. China buys more than 25% of the oil that Saudi Arabia exports. If priced in yuan, those sales would boost the standing of China’s currency.

Until next time...

Thank you for reading this week’s issue. If you found it interesting, please consider sharing it with a like-minded friend or family member.

If you have any questions or feedback, please feel free to reach out!

Have a great week.

Why ‘Buy the Umbrella’?

Individuals, many of whom also run businesses and governments, tend to not think of the downside when the present is stable, and the future is looking positive (usually when we feel most in control).

Just because it is currently sunny, does not mean it will never rain. If we are not prepared, once it does begin to rain, we will end up running around looking for an umbrella in the middle of a storm, when they tend to be in short supply. We therefore need to buy the umbrella before it rains.

At the same time, we cannot allow our awareness of risk to make us fearful, pessimistic, or paranoid, as this too works against us over the long-term.

Having the right mindset in advance is critical. The challenge is getting the right balance between being optimistic about the future and being able to not only withstand future crises, but in fact grow stronger due to the opportunities they tend to present. It is not enough just to be conservative. One needs to be willing to put our cash to work when others feel least comfortable doing it. To do that with confidence, we need to have a foundational understanding of history, business, markets and human psychology.

Our mission at BTU is to learn as much about the world as possible, and in doing so, to try to find investment opportunities with favourable risk/reward characteristics. These should, over the long term, help build sustainable wealth.