'Buy the Umbrella' - Issue #12

Hi there!

Here is your latest dose of “Buy the Umbrella”, a short list of interesting things I’ve been reading and thinking about during the week.

Tweet

Lyn Alden has published a fascinating piece on the self-reinforcing cycle that has enabled the U.S. stock market to benefit from excess global capital. Importantly, Alden examines the potential catalysts that could cause this to reverse.

My favourite takeaways are:

The U.S. stock market currently represents 61% of global stock market capitalisation, despite the fact that U.S. makes up only 23% of global gross domestic product (GDP).

Since the end of the highly inflationary period of the 1970s, the U.S. and the rest of the developed world have been in a four-decade trend of declining interest rates.

The U.S. has reduced its effective tax rate for corporations over the past several decades via declining headline tax rates and an increase in deductions (lobbying helps).

The petrodollar system has given the U.S. a form of Dutch Disease. You can read more in this FT article about how the country discovered that it was the "Saudi Arabia of money".

The U.S. used to be the world’s largest creditor nation until the 1980s and is now the world's largest debtor nation, meaning it has a negative net international investment position.

U.S. households now have record high allocations to equities due to a combination of inflows and valuation increases.

The big question is what happens if some of the above trends pause or reverse?

Quotes

“The magician and the politician have much in common: they both have to draw our attention away from what they are really doing.”

— Ben Okri

"There is only one success... to be able to spend your life in your own way."

Charts

U.S. housing market can endure higher interest rates

Since the global financial crisis in 2007/08, U.S. households have transitioned to fixed-rate mortgages, reducing their interest rate sensitivity that comes with adjustable-rate mortgages. This positive development should reduce default risks for banks and cushion the housing market if interest rates continue their move higher. On the flip side, banks will benefit less from rising interest rates.

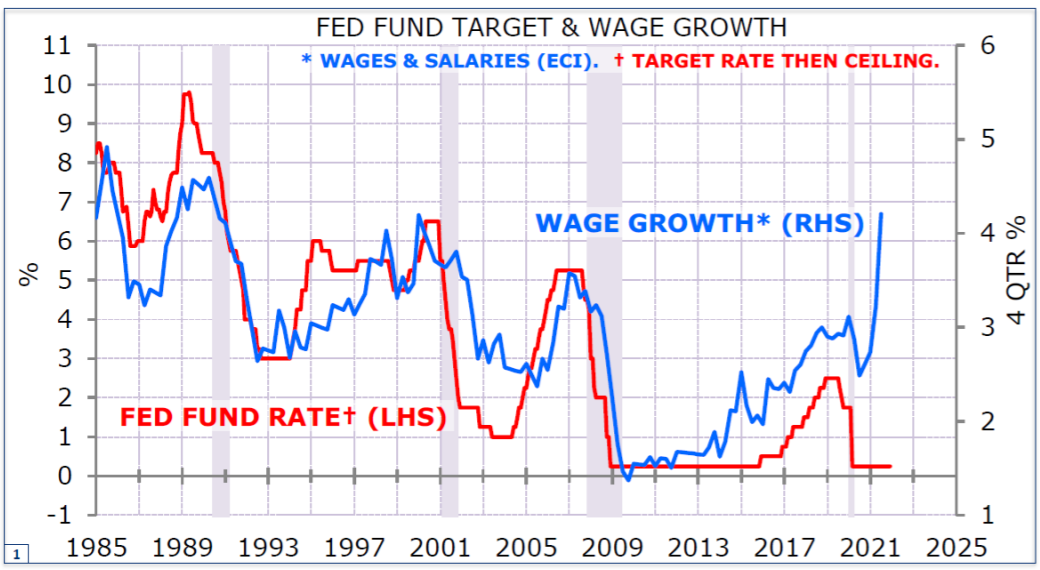

Fed funds and wage growth

The chart below highlights that the federal reserve has historically kept a very close eye on wage growth when setting interest rate policy (i.e. the Fed funds rate).

Interestingly, there has been a divergence in the most recent cycle, where wages have spiked significantly and yet the Fed has kept interest rates at the 0-25bps range. This looks highly likely to change in 2022, with the Fed communicating at least three interest rate hikes this year and three more next year.

Fed funds and the U.S. bond market

Last week, we discussed how some investors believe the fed takes cues from equity markets in the form of a 'fed put'. Another factor that some investors believe influence the fed when it comes to setting its interest rate policy is the U.S. treasury market. As the chart below illustrates, the fed's target rate moves inline with 2-year US treasury yields, which are set by investors.

Notably, the 2-year treasury yield is at around 1%, suggesting the fed is behind the curve and will want to catch-up quickly.

At the start of 2021, investors expected interest rates to remain near zero in 2022 and 2023. Twelve months later, a strong economic backdrop combined with low unemployment and uncomfortable inflation data, has resulted in wall street now believing that four hikes are warranted, with some going as far as suggesting five or more hikes.

J.P. Morgan CEO Jamie Dimon speaking to CNBC last week, believes that it is possible that inflation is worse than people think and that he "personally, would be surprised if it's just four increases this year. Four would be very easy for the economy to absorb".

Dimon goes on to add that "We're expecting that the market will have a lot of volatility this year as rates go up, and people do projections and look at the effects of interest rates on businesses differently than they did before... If we are lucky, the Fed will slow things down and we will have a soft landing".

Articles

EU nations will have to "think about" reining in spending

Senior German finance ministry official, Florian Toncar, said EU nations will have to think about reining in government borrowing and re-imposing budget discipline sooner than expected as markets will start to punish highly indebted states: “I am quite convinced that perhaps very, very soon, Europe won’t ask itself how much debt the rules allow and how much the rules can be bent, but rather how much debt the markets allow”.

Leaders have agreed to suspend the bloc’s fiscal rules until 2023, however there is now debate about whether the so-called 'Stability and Growth Pact' should be reformed to allow more flexibility beyond next year. Previously, Chancellor Olaf Scholz’s coalition government has signalled an openness to reforming the rules, therefore the comments from Toncar, a member of the FDP, marks a shift in tone.

China’s birth rate dropped to a record low

Although mainland China's overall population increased to 1.41 billion people, the National Bureau of Statistics said the birth rate fell to 7.52 children per 1,000 people from 8.52 in 2020. The "shocking" development showed that the rate was the lowest since records began in 1949. There were 10.6m births in 2021 compared with 12.0m in 2020.

“The demographic challenge is well known but the speed of population aging is clearly faster than expected”, Pinpoint Asset Management said. “This suggests China’s total population may have reached its peak in 2021. It also indicates China’s potential growth is likely slowing faster than expected”.

Finance Tip of the Month

People tend to underestimate the power of compounding over a lifetime. Albert Einstein once said “compound interest is the eighth wonder of the world. He who understands it, earns it… he who doesn’t… pays it. Compound interest is the most powerful force in the universe”.

The easiest way to demonstrate its impact is via an example:

Starting with an investment of $1,000 and allowing it to compound, by reinvesting the income it generates, for 30-years at 6%, you end up with $5,743. If you invested for 40 years, you would end up with $10,286.

The table below illustrates the power of compounding at select returns over specific timeframes, assuming you start with $1,000. For those who want to play around with the assumptions, NerdWallet has a handy compound interest calculator.

Until next time...

Thank you for reading this week’s issue. If you found it interesting, please consider sharing it with a like-minded friend or family member.

If you have any questions or feedback, please reach out!

Have a great week.

Why ‘Buy the Umbrella’?

Individuals, many of whom also run businesses and governments, tend to not think of the downside when the present is stable, and the future is looking positive (usually when we feel most in control).

Just because it is currently sunny, does not mean it will never rain. If we are not prepared, once it does begin to rain, we will end up running around looking for an umbrella in the middle of a storm when they tend to be in short supply. We therefore need to buy the umbrella before it rains.

At the same time, we cannot allow our awareness of risk to make us fearful, pessimistic, or paranoid, as this too works against us over the long-term.

Having the right mindset in advance is critical. The challenge is getting the right balance between being optimistic about the future and being able to not only withstand future crisis, but in fact grow stronger due to the opportunities they tend to present. It is not enough just to be conservative. One needs to be willing to put cash to work when others feel least comfortable doing it. To do that with confidence, we need to have a foundational understanding of history, business, markets and human psychology.

Our mission at BTU is to learn as much about the world as possible, and in doing so, to try to find investment opportunities with favourable risk/reward characteristics. These should, over the long term, help build sustainable wealth.